Oregon’s Changing Economy: An Economist View by The Oregon Ledger

Three Months, Two Forecasts, One War

Eric Fruits is an economist based in Oregon and has spent much of his career working on state and local public policy issues in Oregon. Over the years, he has written and testified on issues ranging from taxation and education to pensions, regulation, and the regional economy.

Eric writes for The International Center for Law & Economics and publishes his own work on his substack: ericfruits.substack.com

Oregon’s Changing Economy: Three Months, Two Forecasts, One War

Lawmakers may be excited that Oregon state revenues are up. But, take out the legislature’s tax increases, and the economy went backward.

Oregon’s Office of Economic Analysis puts out four economic forecasts a year. Usually, the changes from one quarter to the next are modest—updated tracking numbers, minor revisions, the kind of thing only budget watchers and weirdos like me pay any attention to.

Three months isn’t very long. So, quarter-to-quarter forecast changes are fairly ho-hum affairs. Looking for changes is a bit like those “spot the difference” cartoons that used to be in the Sunday paper’s comics section.

But this time—from the February forecast to the May forecast—it is different. Quite a bit different. And the biggest reason is a war in the Middle East that nobody in Oregon has much control over, but should remind us we live in a great big world where events abroad can affect us in our tiny northwest corner of the country.

Back in February, the mood was cautious but improving

The March forecast—actually released in early February—carried something the state’s economists hadn’t had much of lately: a degree of optimism. And by “degree,” I really mean “a tiny bit.”

Oregon had been losing jobs throughout most of 2025. Year-over-year job losses outside a recession are unusual in this state. The March forecast said the losses should start turning around. The baseline projected employment would grow about 0.6% in 2026, and unemployment would hover around 5.3%. The recession odds were 20%.

The General Fund was tracking toward a projected ending balance of just under $200 million. Sure, that’s a positive number, but darn close to zero, considering the size of the General Fund—$35.7 billion in revenues for the 2025-27 biennium.

The big question heading into 2026 was whether the national economy—which had grown at surprisingly strong rates through the middle of 2025—would carry that momentum into Oregon’s labor market. That was the question the March forecast was sitting with, noting “open questions remain” regarding “labor market malaise” and inflation.

Then Iran

About three weeks after the March forecast was released (remember, it was released in February), the United States and Israel commenced military operations against Iran. Traffic through the Strait of Hormuz—which handles a large share of global oil shipping—was severely curtailed. Oil prices spiked.

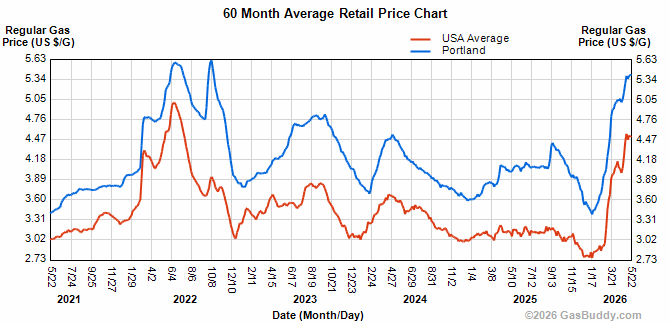

Crude oil, which had averaged around $69 a barrel through 2025, is now more than $100. Gasoline at the pump—which had actually been below year-earlier levels in January, around $2.80 a gallon—crossed $4.50 by early May.

Lower- and middle-income households feel that most. Fuel spending takes a bigger share of their budgets. They can’t easily cut back on gas. So they cut back on other things. And the businesses that serve them start to feel it.

S&P Global, which provides the national economic modeling that feeds into Oregon’s forecast, cut its projected 2026 GDP growth from 2.2% to 1.6% between January and May. That’s a meaningful revision.

Is Oregon heading into a recession?

OEA doesn’t think so. The office estimates we’d need nationwide gasoline prices to stay above about $5.50 a gallon—a dollar above current prices—before recession risks become genuinely serious. The May recession probability ticked up to 22% from 20% in the March forecast. That’s an uptick, but not a red alert.

But here’s what it means for Oregon: that anticipated labor market turnaround has been pushed further off. The 2026 employment forecast flipped from a 0.6% annual gain to a 0.6% decline. That’s a swing of roughly 30,000 fewer jobs through the year than March had projected—and we’ve already lost more than 10,000 jobs since the end of last year. OEA forecasts the unemployment rate will reach 5.4% by year-end.

The revenue headline, and what’s inside it

Here’s where things get a little counterintuitive. Stay with me, folks.

The May General Fund forecast is up $345 million from the March forecast. The projected biennium ending balance improved from about $198 million to about $345 million. If you stop at the headline, it sounds like Oregon’s fiscal situation got materially better, but policymakers need to understand how much of this is due to legislative actions versus economic conditions.

It got somewhat better. But not primarily because of the economy.

Of that $345 million improvement, $368 million came from the 2026 short legislative session. Oregon disconnected from a couple of federal tax provisions in H.R. 1, also known as the One Big Beautiful Bill. This disconnect includes rules around business depreciation and a jobs tax credit, which will boost anticipated corporate income tax receipts. Changes to personal income tax treatment added more. A pair of fund sweeps rounded it out. Put simply, the legislature improved the state’s fiscal situation through tax increases rather than economic growth.

Strip out the legislative changes, and the underlying picture is actually slightly worse than March projected—about $23 million below that forecast. Revenues from February through April also came in $308 million short of first quarter expectations.

OEA says most of that is timing: companies delayed estimated tax payments while waiting on a state program that wasn’t renewed until late March, and the usual distortion that comes from a large kicker credit affecting when people file. Most of those dollars are expected to show up later in the biennium.

One more thing: the legislature also increased spending by $198 million for the biennium. So while the ending balance improved, it improved by less than half of what the headline revenue gain suggests.

A shift in where the money is coming from

The April income tax filing deadline gave OEA its first real look at 2025 income—and there was a notable shift in the pattern. Wage income grew more slowly than expected. Capital gains, dividends, and retirement distributions came in much stronger.

That matters for two reasons. Capital income is concentrated at the top of the income distribution, which means a higher effective tax rate under Oregon’s graduated structure, so it’s a modest revenue positive. But it’s also less stable than wages. Capital income can shrink quickly when markets turn, introducing greater uncertainty into forecasts and highlighting potential vulnerabilities in Oregon’s revenue stability.

Oregon’s semiconductor and electronics manufacturing sector—centered in Washington County—is projected to lose roughly 12-13% of its jobs in 2026, on top of a similar decline in 2025. Oregon manufacturing employment is down 9.8% from pre-COVID levels. In contrast, U.S. manufacturing is down only 1.2%.

What to watch

The May forecast assumes oil prices ease over the coming year. If the Iran conflict winds down and energy costs fall back, Oregon’s employment picture improves faster. If it doesn’t, the 22% recession probability will tick up, and Oregon may be one of the first states to face it. Remember, Oregon does not have a good track record of dealing with recessions.

The Federal Reserve, widely expected to resume cutting rates in 2026, is now on hold through at least mid-2027—and a rate increase by year-end is being discussed. Long-term interest rates are near their highest levels since 2007. For Oregon’s housing market, already under pressure before any of this happened, that means the wait for relief continues.

The next forecast is scheduled for September. By then, the outstanding questions about 2025 income will be largely resolved, second-quarter GDP data for Oregon will be available, and the oil market will have either calmed down or gotten worse.

The March forecast asked whether Oregon’s growth story was about to improve. The May forecast answered: not yet, and maybe not.

You might want to build up that rainy day fund, because the clouds are still in the sky.

Do you have a story for The Inquirer? Email: editor@corvallisnow.com

→ Support us

We’ll keep it ad-free even if you don’t.